When monitoring live currency grids, it is easy to assume that the numbers flashing across your screen reflect a unified global value. Developing traders frequently believe that every market participant sees the exact same transaction costs at any given second. The reality is that the financial layout of your execution relies heavily on the specific plumbing of your platform. Behind those tight decimal quotes sits a massive, ultra-fast network of institutional relationships that brokers navigate continuously to source global liquidity.

What does “liquidity” actually mean in the retail currency market?

In the context of retail currency trading, liquidity represents the immediate availability of buy and sell orders at any given price coordinate. The market operates on a split auction layout, separating what a buyer offers from what a seller demands. The bid price is the absolute highest rate a buyer will pay to absorb your position, while the ask price is the lowest rate a seller will accept to hand over an asset.

The distance between these boundaries forms the spread, which functions exactly like a non-negotiable service fee or an entrance toll that you are forced to cross every time you enter a live market setup. When liquidity is thick, thousands of matching orders flood the ledger every second. This deep volume pushes the bid and ask numbers closer together, compressing your transactional costs down to structural minimums.

Where do premier brokers look to find this institutional supply?

Retail firms do not generate currency pricing out of thin air; they must source it directly from massive global financial intermediaries known as Tier-1 liquidity providers. This elite group includes multinational investment banks like JPMorgan Chase, Deutsche Bank, Citibank, and Barclays.

These institutions handle the massive institutional money flows generated by international corporations, hedge funds, and governments. Because these banking desks control hundreds of billions of dollars in daily order volume, they quote the tightest raw wholesale prices in existence. Partnering with a competitive network of low spread forex brokers ensures your trading terminal links directly into these premium banking streams, letting you tap into the deepest financial reservoirs in the world from your personal desk.

How does a price aggregation engine compress the visual spread?

If an intermediary relies on just a single global bank for its price feeds, its clients are entirely vulnerable to that individual bank’s pricing choices. To circumvent this limitation, premier brokers deploy an advanced software tool known as a price aggregation engine.

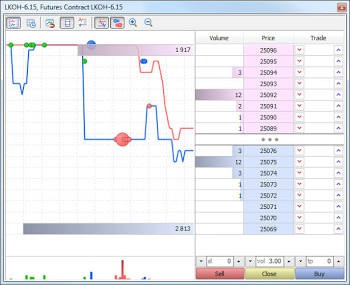

Analyzing the structural layout of market depth within a terminal order book. Source: MetaTrader 5

This technology functions exactly like an automated comparison-shopping scanner, pulling live price quotes from dozens of global banking desks simultaneously. The aggregator automatically isolates the absolute highest available bid from Bank A and pairs it with the absolute lowest available ask from Bank B. By unbundling these independent banking feeds and weaving them into a singular, centralized order book, heavy institutional competition strips away artificial premiums. The visual spread on your terminal collapses to razor-thin fractions of a pip.

What role does a liquidity bridge play in processing my trade?

Your user-facing terminal is excellent at charting price history, but it does not possess a native connection to the global interbank financial network. That critical link is handled by specialized institutional middleware known as a liquidity bridge or execution gateway.

When you fire a market order, the bridge instantly translates your ticket into FIX (Financial Information eXchange) protocol—the standardized language spoken by global investment banks. Deploying your active strategies through a sophisticated, enterprise-grade terminal, such as the best forex broker for mt5, ensures your software communicates with the liquidity bridge without processing latency. This high-speed integration allows your orders to slice through global aggregation nodes in milliseconds, catching the tightest wholesale fills before quotes can slip away.

Why do variable spreads still expand during high-impact news drops?

The electronic order ledger behaves exactly like a live thermometer for market risk, meaning it responds instantly to shifting macroeconomic conditions. When a high-impact announcement—like a central bank interest rate shift—hits the wires, global institutional banks face immense pricing uncertainty.

To protect their corporate capital from sudden, erratic price gaps, algorithmic liquidity desks quickly pull their resting limit orders out of the matching ledger. This sudden programmatic retreat leaves a hollow order book behind. When an incoming retail market order hits this empty ledger, the platform has to travel across multiple sparse pricing layers to find a match. The active spread expands defensively like a rubber band, and even the most advanced infrastructure cannot force banks to quote tight pricing during a market panic.

Practical Action Plan

Stop evaluating brokerage offerings based purely on superficial marketing promotions or loud landing pages. Review your execution history statements from the past month, check the exact pips you are paying across different session hours, and ensure your strategy runs during peak volume overlaps. By restricting your high-volume market execution exclusively to the London and New York session crossover when the price aggregator engines are backed by maximum banking competition, you can naturally minimize your transactional drag and trade with complete mathematical clarity.